How do interest rates affect the share market?

Rising interest rates – a phrase that we have heard a lot of lately. But the Reserve Bank of Australia is on a rate-rise tear to combat record-high inflation and slow the pace of economic growth, following in the footsteps of Central Banks around the world.

We’ve been hearing a lot about the impact the higher rates are going to have on the property market, but we haven’t heard too much about the impact on equity markets. But to be blunt, interest rates have an enormous impact on company earnings and equity markets – as everyone participating in the US market has seen this year. Alongside rising rate expectations has come increased volatility and negative returns as investors price in rate rises, reassess growth expectations and refocus on the fundamentals.

Changes in interest rates can impact companies and equity market performance in several ways. As interest rates rise, debt servicing costs increase and squeeze profits. Valuations, especially for growth sectors like technology, can be battered by a jump in rates. Finally, higher rates curb inflation by slowing the economy, an important source of profit for companies.

Here we explain the impact of rising rates on equity markets. We also uncover the sectors best positioned to keep their heads above the rising water.

Why are interest rates rising?

During the pandemic, central banks around the world lowered rates to encourage consumer spending and credit growth on hope of stimulating the economy. However, record low rates over the last two years have caused demand to outpace already stressed supply resulting in soaring inflation.

The Reserve Bank joined compatriots in the US, New Zealand, Canada and the United Kingdom in raising rates earlier this month. Investors expect multiple additional rate hikes from central banks this year.

Relationship between rates and equities

As interest rates rise, the cost for companies to borrow money increases.

Whether companies borrow money from a bank in the form of a business loan or they sell fixed income products such as corporate bonds to bring in cash, rising rates mean everything costs more.

Each dollar companies use to service debt is a dollar that will not be counted in net profits, and a dollar that won’t be paid out to shareholders in the form of dividends.

Businesses with higher returns on capital can typically fund their operations from existing cash flows, and therefore have less need for debt. In contrast, debt-intensive companies typically have lower returns on capital, meaning they may have inadequate cash flow to support their operations. This can be exacerbated by rising inflation, which could see rises in funding costs, leases, wages etc.

Why are tech stocks being hit harder?

Generally, when interest rates are low, future profits are valued more highly. Conversely, when interest rates rise, promises of future profits become less valuable. This dynamic between interest rates and future profits weighs most heavily on new and growing companies where most profits are still years away, most emblematically in the technology sector.

The process of determining the fair value of a stock is called valuation. The most common valuation method is the discounted cash flow model (DCF). The main idea behind a DCF model is relatively simple: a stock’s worth is equal to the present value of all its estimated future cash flows.

Let’s do a quick example to show how changing interest rates affects the future value of a company’s profits.

With an interest rate of 2%, a company forecast to make $1,000 in 10 years has a present value of $980.39. When the interest rate is at 8%, the same company in 10 years’ time only has a present value of $925.93.

The relationship between interest rates and company valuation weighs heavier on the technology sector. Some companies in the sector are making a loss to chase growth for future profits. As such, they are more heavily impacted in their valuation as their cash flows don’t exist until further in the time horizon.

Others had massive valuations placed on them during the pandemic as investors hunted for companies that would best weather the storm. These expectations are now coming off as investors price in slowing economic growth and rising interest rates.

A significant part of the value of technology stocks is their future earnings profile, and as investors lower their growth expectations and/or discount those future earnings at a higher rate, the present value for these stocks fall further and faster than the broader market. In addition, market sentiment has turned negative on growth stocks, especially after Netflix (NFLX) fell off a cliff, dropping over 20% in one day following its earnings release.

The dynamic between rates and valuation has been observed over the past year in the technology sector with the NASDAQ-100 Technology Sector Index falling 21% since January. The relationship can also be observed in Australia and has cost some market darlings. Block, REA Group and Xero are all down 35%, 37% and 41% respectively over this year.

A slowing economy and consumer confidence

As central bankers increase interest rates to curb inflation, they also induce a behavioural shift in consumer sentiment to reduce their spending. This is an issue for companies that are reliant on low-interest rates, strong economic growth and high consumer confidence.

For example, when unemployment and interest rates are low, consumers are optimistic about the future and spend more of their hard-earned money on goods and services they desire, like dining out or a new TV. However, as rates rise and the cost-of-living increases, consumers become pessimistic and cautious about the future. Their focus has shifted from buying a new iPhone to managing their mortgage. They are more likely to continue to wear the shoes they already own rather than fork out an extra $200 for the newest kicks. This poses a threat for companies that fall in the “consumer discretionary” sector and cater to consumer wants as opposed to needs.

It’s not all bad news

Interest rates rising may harm certain sectors of the market, but this isn’t true for all sectors. In fact, there are some sectors that benefit from higher interest rates such as financials. As rates rise, the wider the bank margins become.

Banks are successfully able to pass on cash rate rises to borrowers by increasing the rate of interest on loans while being able to fund themselves at a cheaper rate as savers rush to deposit their savings.

This can be observed earlier this month after the RBA raised the cash rate for the first time in over 10 years.

Australia’s big four banks wasted no time matching the Reserve Bank’s cash rate, each hiking their variable home loan rates.

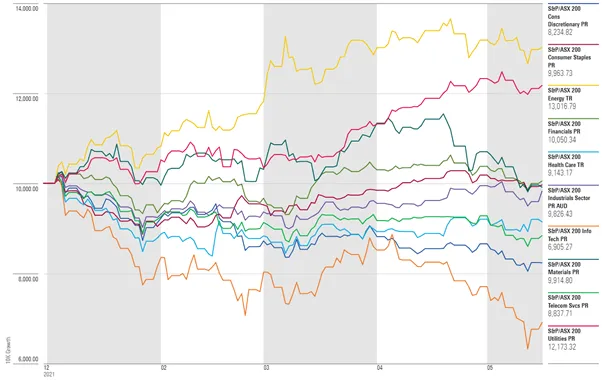

Growth YTD | ASX Sectors

Not only do certain sectors benefit from higher interest rates but different asset classes also benefit.

Using the banking example above, all of Australia’s big four banks also increased their savings rate. This incentivises investors to increase their cash holdings as they receive higher returns.

Moreover, bonds and interest rates have an inverse relationship. When interest rates rise, the price of bonds falls making the asset look more attractive to investors.

If you would like to review your existing portfolio, or if you recognise that now might be a good time to establish a strategy, please feel free to contact us here.